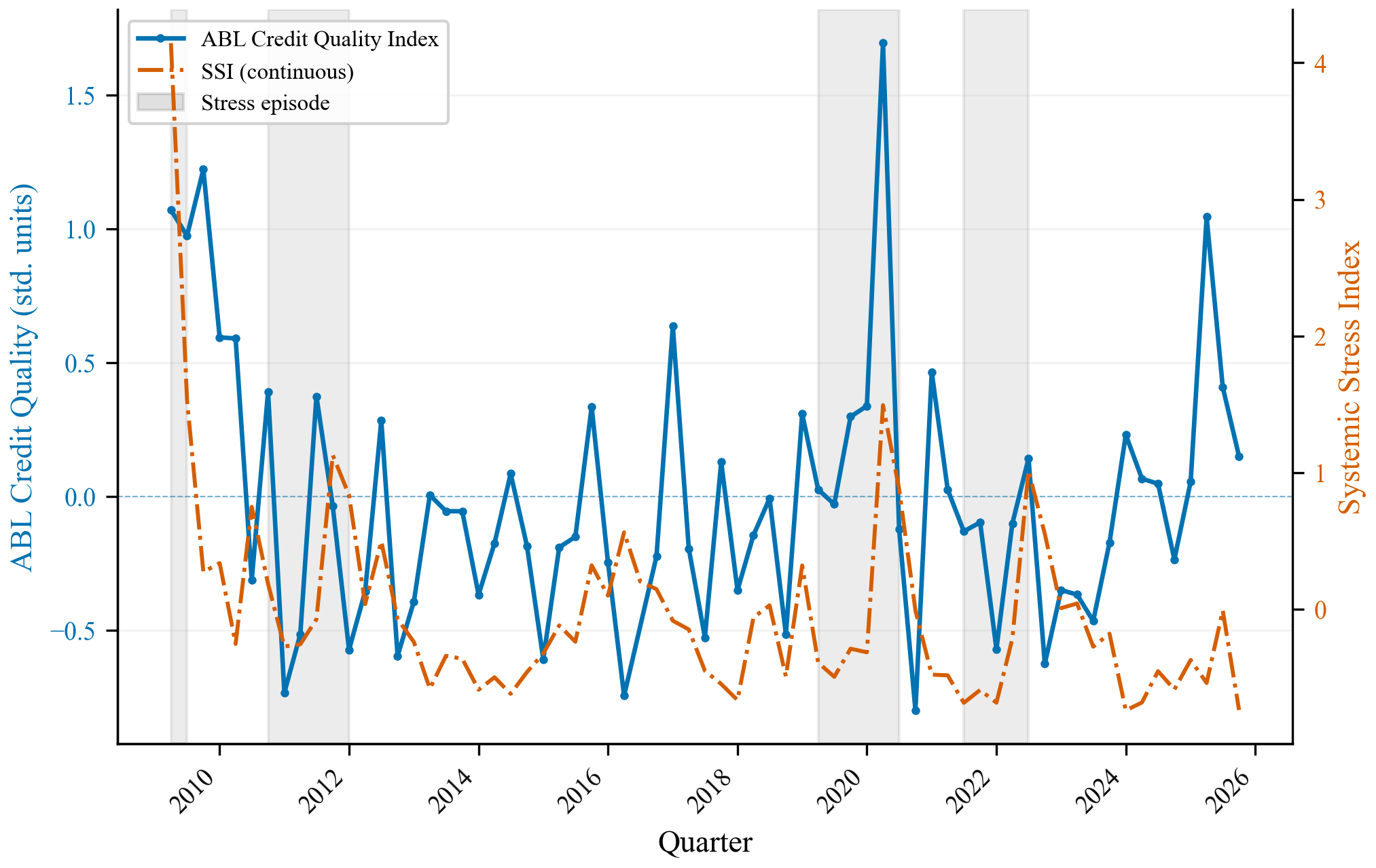

Figure: Standardised ABL Credit Quality composite (blue) typically leads the Systemic Stress Index (orange dashed) by 1–4 quarters into stress episodes (shaded). 2009Q1–2025Q3.

We show that asset-based lending (ABL) survey data predict systemic financial stress. From the quarterly surveys of the U.S. secured-lending industry (2009–2025), we construct a composite of private, lender-reported credit-quality indicators. Out of sample, adding the ABL composite to a standard macro-financial control set raises twelve-month-ahead crisis discrimination from an AUROC of 0.67 to 0.73. The predictive content is horizon-dependent: at longer horizons, lenders’ private survey assessments outperform secondary-market ABS prices, consistent with confidential lender information leading market prices; the edge narrows at shorter horizons. The long-horizon signal is robust to controls for bank-lending standards, financial-conditions indices, and bank-level delinquencies. We establish ABL lender surveys as a novel class of leading systemic-stress indicators, complementary to the macro-financial early-warning literature.

| Finding | Estimate | Detail |

|---|---|---|

| ABL credit quality — in-sample | coef. 1.324*** | Predictive logit at 1-quarter horizon; most significant ABL predictor. Pre-stress mean fitted probability 46% vs 3.1% at non-stress quarters. |

| ABL credit quality — out-of-sample | +6.2 pp | Out-of-sample AUROC rises 0.670 → 0.732 at 12-month horizon under strict expanding-window protocol (43 held-out quarters, no look-ahead). |

| Long-history bank-channel validation | 0.82–0.96 | FR Y-9C call reports, 2000–2025 (50,031 BHC-quarters; 1,238 bank holding companies). AUROC range across forecast horizons; comparable to established macro EWS benchmarks. |

| Private information — 24-month horizon | +1.4 pp (SFNet leads) |

SFNet-only AUROC 0.856 vs TRACE-only 0.842. Lenders’ private survey assessments carry forward-looking information not yet in secondary-market ABS prices. |

| Private information — 12-month horizon | −1.6 pp (TRACE leads) |

SFNet-only AUROC 0.683 vs TRACE-only 0.699. Market prices catch up as a crisis approaches; the private-information premium is concentrated at longer horizons. |

*** p < 0.001. AUROC: area under the ROC curve (0.5 = no information; 1.0 = perfect). Stress defined as top-decile ABL Stress Index exceedances (p90 threshold); 7 stress quarters in the sample. H1 uses window-4 (12-month) target; H2 compares full SFNet-only vs TRACE-only feature sets on the extended-control panel.

ABL lenders observe covenant violations, field-exam outcomes, and watch-list reclassifications in real time. This private credit intelligence leads macro-financial aggregates by 2–4 quarters, giving ABL survey data incremental predictive power at the policy-relevant 12-month horizon.

At 24 months, lenders’ confidential assessments hold an information advantage over ABS prices (+1.4 pp AUROC). By 12 months the advantage reverses slightly as market prices incorporate the same signals, consistent with price discovery completing as crisis approaches.